Is Rent Vesting Dead? A straight-talking banker and broker's view

- Kevin Leong

- Jun 12

- 2 min read

No, but it's changed. Here's what you actually need to know.

Rent vesting means renting where you want to live and buying where you can afford and where the

numbers make sense. It's been a popular strategy for people who can't yet buy in their dream suburb but

don't want to sit on the sidelines doing nothing.

The engine behind it has always been negative gearing, the ability to offset investment property losses

against your income tax. That tax benefit helps you borrow more and keeps holding costs down. Recent

budget changes have tightened things, but they haven't killed the strategy. Here's the honest picture.

What the budget changes actually mean

The headline sounds alarming. The reality is more nuanced. Properties already negatively geared are

protected. And critically, new builds still qualify for the full tax benefits which means buying brand-new

property in the right location still works very well for rent vesters.

Where it gets harder is for new investors buying established properties. The tax offset has been reduced or

removed depending on your situation, which directly cuts your borrowing power.

"The budget changes raised the bar, they didn't close the door. For the right buyer, in the right property, rent vesting still stacks up."

The risks you need to know about

How to navigate it if you're new to this

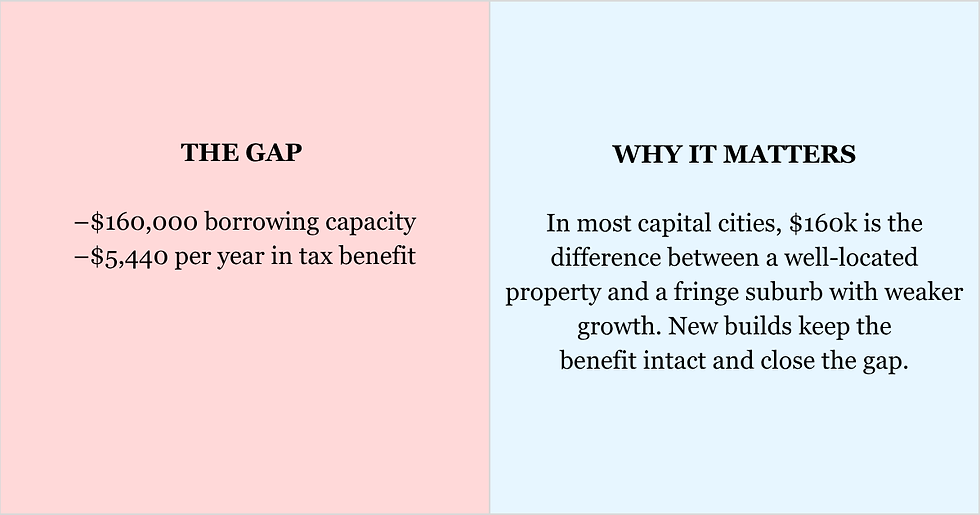

1. Look at new builds first: They retain negative gearing benefits and can close the borrowing gap.

2. Use a buyer's advocate: Local knowledge spots growth areas before the market prices them up.

3. Get your finance sorted before you search: Your borrowing limit shapes every other decision.

4. Engage a good property manager from day one: They protect your yield and catch problems early.

5. Think long term: Policy noise matters far less than a well-chosen asset held for a decade.

THE WORKED EXAMPLE

$120,000 income: borrowing capacity with vs without negative gearing

Illustrative only — based on standard lender serviceability models. Individual results vary with lender policy, existing debts, living expenses (HEM) and loan structure. Not financial or tax advice.

Our view at Lendcap

We've helped clients build real wealth through rent vesting, people who lived where they loved while quietly

growing equity in properties they'd never call home. The rules have shifted but the opportunity hasn't gone

away. What's changed is that the margin for error is smaller, which is exactly why getting the right advice

matters more than ever.

We don't just arrange your finance. We connect you with a curated network of buyer's advocates and

property managers who can help you make the right call, from the first search through to settlement and

beyond. Speak to Lendcap to find out where you stand.

General Advice Disclaimer

The information provided in this article is general in nature and does not take into account your personal objectives, financial situation, or needs. It should not be considered financial, tax, or legal advice. You should seek professional advice tailored to your individual circumstances before making any financial decisions.

To understand what options may be suitable for your situation, book a consultation with Lendcap today.

Comments